Calculating amounts available for distribution

The Company’s Board of Directors is obligated to declare the distribution of net income from the preceding fiscal year, subject to review and deliberation by shareholders.

Per Brazilian Corporate Law, net income is delineated as the fiscal year’s result, subtracting any accumulated losses from prior years, alongside provisions for income tax, social contribution tax, and employee and administrator profit sharing.

The net profit calculation and the allocation to reserves in any given fiscal year are determined based on the company’s audited and consolidated financial statements for the prior fiscal year.

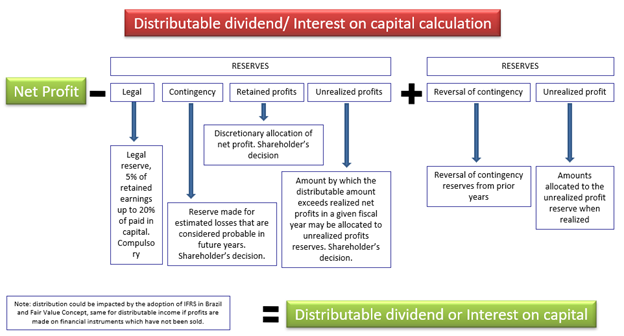

According to Brazilian Corporate Law, the amount corresponding to net profit, as adjusted, is available for distribution to shareholders in any fiscal year, and may be:

• Decreased by allocations to the legal reserve.

• Decreased by allocations to statutory reserves, if applicable.

• Decreased by allocations to the contingency reserve, if applicable.

• Decreased by allocations to the retained profit reserve, if applicable.

• Decreased by allocations to the unearned profit reserve.

• Increased by the reversal of contingency reserves recorded in previous years.

• Increased by amounts allocated to the unearned profit reserve upon realization, if not offset by losses.

The allocation of profit to the statutory reserves and of the unearned profit reserve may not be approved in a fiscal year if it prevents the distribution of the mandatory dividend.

What about reserves?

According to Brazilian Corporate Law, companies generally present three main reserve accounts: (1) retained profits reserves; (2) legal reserves and (3) capital reserves. Contingency and unearned profit reserves are discretionary.

• Reserves of Retained Profits: According to Brazilian Corporate Law, shareholders, following a proposal from the management team, can decide in a shareholders’ meeting to retain a portion of the net income, as outlined in an approved capital expenditure budget. The allocation to retained earnings cannot occur before the payment of the mandatory dividend. The total of profit reserve accounts, excluding contingencies, must not surpass the company’s capital stock. If it does, a shareholders’ meeting will be convened to vote on whether the excess should be used to pay subscribed and unpaid capital, increase the capital stock, or distribute dividends.

• Legal Reserves: Companies are obligated to maintain a legal reserve, to which they must allocate 5.0% of their annual net income until the cumulative reserve equals 20.0% of the paid-in capital. However, no allocations are required in a year when the legal reserve, combined with other established capital reserves, exceeds 30.0% of the capital stock or is used to offset losses. Shareholders must approve the amounts assigned to this reserve in a shareholders’ meeting, and such allocations can only be utilized to increase the capital stock, making them unavailable for dividend payments.

• Capital Reserves: According to Brazilian Corporate Law, capital reserves consist of goodwill (ágio) reserves from share subscriptions. For companies listed on the Novo Mercado, capital reserves serve specific purposes: absorbing losses exceeding accumulated earnings and profit reserves, redeeming, repaying, or buying common shares, and increasing share capital. These reserves encompass premiums, tax incentives, and grants for investments. Amounts allocated to capital reserves are excluded from the mandatory dividend calculation.